The Era of Software-Defined Leases

Accessing Advanced Mobility Without the Upfront Cost

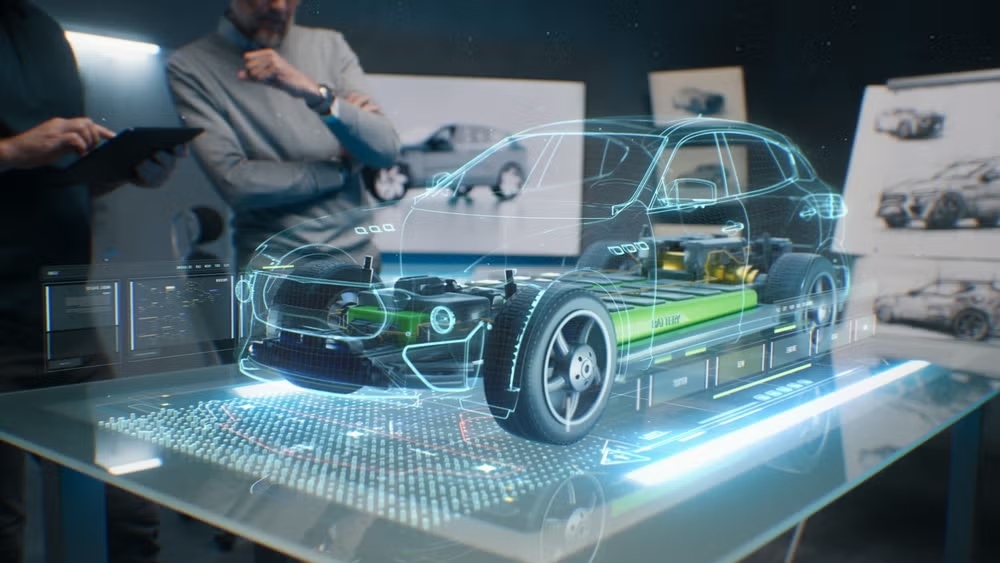

The traditional concept of leasing—borrowing a physical asset for a set period—is undergoing a radical transformation. We are moving away from agreements based solely on the depreciation of metal and rubber toward models centered on access to cutting-edge experiences. Modern agreements increasingly package sophisticated driver-assistance systems and hands-free automation that would be prohibitively expensive to purchase outright. For many consumers, the lease is no longer just about the car; it is about securing the rights to utilize the latest safety protocols and autonomous features that dramatically reduce driver fatigue during long commutes.

This shift is inextricably linked to the rapid electrification of the automotive sector. Electric platforms integrate seamlessly with electronic control units, allowing for the smooth implementation of automated parking and sensor fusion technologies. These features do more than provide convenience; they communicate with infrastructure to preemptively mitigate accidents. For the consumer, the lease becomes a gateway to perpetually updated safety standards. Rather than owning a vehicle that becomes technically obsolete within years, leasing provides a flexible pathway to transition between technological generations, effectively turning the driver from an owner of hardware into a subscriber of mobility innovation.

Continuous Evolution Through Remote Connectivity

Historically, a leased vehicle was at its peak performance the moment it left the dealership lot, followed by a slow decline in capability and value. This trajectory is being upended by wireless software integration. The widespread adoption of remote system updates allows vehicle operating systems to be refreshed and improved without physical intervention. Much like a smartphone that updates overnight, modern leased vehicles can acquire new functionalities, refined user interfaces, or improved energy management algorithms while parked in the driveway.

This capability fundamentally changes the maintenance equation for lessees. Previously, updating navigation maps or tweaking control modules required scheduling appointments and losing hours at a service center. Now, these enhancements occur in the background, minimizing downtime and "admin" stress for the user. More importantly, this dynamic helps combat the feeling of driving an aging model. By keeping the infotainment and powertrain logic current, the vehicle maintains a sense of "freshness" throughout the contract term. This continuous renewal shifts the value proposition: you are not just renting a static machine, but engaging with a platform that adapts and improves over time.

| Feature Category | Traditional Leasing Model | Modern Software-Defined Leasing |

|---|---|---|

| Vehicle Evolution | Performance degrades or remains static over time. | Features improve via remote software updates. |

| Maintenance | Requires physical dealership visits for system tweaks. | Critical patches and upgrades occur wirelessly. |

| Value Perception | Defined by hardware condition and mileage. | Defined by software currency and feature sets. |

| User Experience | "New car smell" fades; tech feels outdated quickly. | Interface and capabilities stay current throughout the term. |

Navigating the Data Dilemma

The Privacy Cost of Connectivity

As vehicles transform into sophisticated data-gathering nodes, the implications for personal privacy within a lease agreement have become increasingly complex. Modern connected cars monitor far more than just odometer readings; they track precise location history, acceleration patterns, and even driver behavior quirks. In a leasing or sharing scenario where the user does not hold the title to the vehicle, the transparency regarding who owns this data—and how it is utilized—often remains murky.

The stakes are raised further in peer-to-peer sharing models or flexible subscription services. When detailed usage logs are stored on cloud platforms, there is a legitimate concern regarding the granularity of the data being archived. The record of where a driver went, when they stopped, and how fast they drove creates a digital fingerprint of their daily life. While this connectivity offers convenience, such as seamless keyless entry and authorized user management, it opens the door to potential profiling. Consumers must now weigh the convenience of digital integration against the risk of their behavioral data being analyzed or shared with third parties without explicit, informed consent.

Securing Digital Rights in Contracts

The digitization of the contracting process itself introduces new layers of vulnerability. While signing a lease via a smartphone app offers undeniable speed, it often creates a disconnect between the user and the fine print regarding data governance. During periods of economic fluctuation, automated vetting processes using digital financial footprints can become more stringent, potentially affecting access to mobility based on algorithmic decisions.

Furthermore, dispute resolution clauses in these digital-first contracts warrant close scrutiny. Some modern agreements include terms that mandate arbitration, effectively waiving the lessee's right to pursue legal action in court should a privacy breach occur. To counter these imbalances, the industry is seeing the theoretical rise of "data cooperatives"—structures where users collectively manage their data rights to negotiate better privacy terms with manufacturers. Additionally, advancements in encryption allow for necessary data analysis without exposing raw personal identifiers. Prospective lessees must look beyond the monthly payment and rigorously evaluate the data protection standards embedded in their digital contracts.

Modernizing Financial Liabilities

Telematics and Personalized Premiums

The intersection of leasing and insurance is being rewritten by the ability to measure risk in real-time. Traditional insurance relied on static demographics—age, zip code, and credit score—to estimate risk. Today, the integration of telematics allows for premiums based on actual driving performance. For a leaseholder, this means that demonstrating prudent driving habits, such as smooth braking and adherence to speed limits, can directly translate into lower monthly operational costs.

This is particularly relevant for the "pay-per-mile" insurance model, which is gaining traction among those with predictable or low-mileage driving patterns. Since lease agreements already impose mileage caps, aligning insurance costs with these limits is a logical financial move. The vehicle’s internal systems automatically verify distance traveled, eliminating the need for manual reporting. For the weekend driver or the remote worker, this ensures that they are not subsidizing the risks of high-mileage commuters. However, this financial benefit comes with the caveat that the driver must be comfortable with the constant monitoring required to validate their "safe driver" discount.

| Scenario | Recommended Insurance Approach | Primary Benefit |

|---|---|---|

| Low Mileage / Remote Work | Pay-Per-Mile / Usage-Based | Cost aligns strictly with actual distance driven; no waste. |

| High Tech / EV Lease | Performance-Based Telematics | Offsets higher repair costs of tech-heavy cars via safe driving rewards. |

| Traditional Commuter | Standard Fixed Premium | Predictable budgeting without the need for constant behavioral tracking. |

The Challenge of Technological Obsolescence

A critical, often overlooked aspect of leasing modern electric and high-tech vehicles is the accelerated rate of "tech depreciation." Unlike internal combustion engines, which have a predictable decay curve, EVs function closer to consumer electronics. Rapid advancements in battery density and charging speeds can render a vehicle released just three years ago significantly less desirable on the secondary market. This potential for obsolescence creates a risk for the residual value—the estimated value of the car at the end of the lease.

For leasing companies, this volatility is compounded by rising borrowing costs. If a vehicle's technology becomes outdated quickly, its resale value plummets, disrupting the financial model that keeps monthly payments low. Consequently, we are seeing a shift where the risk of owning rapidly aging technology is too high for individual buyers, making leasing the safer financial hedge. By leasing, the consumer transfers the risk of battery degradation and technical irrelevance back to the finance company. However, this also means that consumers must be strategic, looking for contracts that acknowledge these risks and perhaps offer flexibility in upgrading as the technology landscape shifts beneath their feet.

Q&A

-

What are the benefits of over-the-air updates in car leases?

Over-the-air (OTA) updates in car leases allow for the seamless enhancement of vehicle software without needing a physical visit to a service center. This can improve the vehicle's performance, add new features, and fix security vulnerabilities, ensuring that the car remains up-to-date throughout the lease period. This can also increase convenience for lessees, as updates can be performed remotely, saving time and effort.

-

How does data privacy impact leased cars, and what measures can be taken to protect it?

Data privacy in leased cars is crucial as modern vehicles collect and store vast amounts of personal data, such as location history and driving habits. To protect this data, lessees should inquire about the leasing company's data management policies, ensure the use of strong, unique passwords, and regularly update software to safeguard against potential breaches. Additionally, understanding how data is shared with third parties is essential to maintaining privacy.

-

What role does usage-based car insurance play in a car lease?

Usage-based car insurance, often referred to as pay-as-you-drive insurance, calculates premiums based on actual driving behavior and mileage. In the context of a car lease, this type of insurance can offer more personalized and potentially lower premiums for lessees who drive fewer miles or exhibit safe driving habits. This can make leasing a more financially attractive option for individuals who do not drive extensively.

-

How can tech depreciation affect car leases, and what should lessees consider?

Tech depreciation refers to the loss in value of a car's technological features over time, which can impact the residual value of a leased vehicle. Lessees should be aware that rapid advancements in automotive technology could lead to quicker obsolescence. When entering a lease agreement, it's essential to consider the potential depreciation of tech features and negotiate terms that account for this, such as shorter lease periods or clauses that allow for upgrades.

-

What should be included in future-proof car lease contracts to protect lessees?

Future-proof car lease contracts should include provisions for technology upgrades, flexible terms for integrating new innovations, and clauses that address the potential obsolescence of current features. These contracts should also consider the potential for regulatory changes affecting autonomous driving and emissions standards. By ensuring these elements are covered, lessees can protect themselves against unforeseen changes and maintain the value and relevance of their leased vehicle.